Analysis updated to June 2026

Disclaimer

The information contained in this document is for educational and informational purposes only. It does not constitute an offer, recommendation, or financial, investment, legal, or tax advice. The opinions expressed reflect personal analysis and may be subject to change without notice.

Investing in financial markets involves risks, including the potential loss of all invested capital. Each reader or investor is responsible for conducting their own research and, if necessary, consulting with a registered financial advisor before making any investment decisions.

The author assumes no responsibility for any losses or damages arising directly or indirectly from the use of the information presented here.

Summary

Palantir is one of the most interesting, and at the same time one of the most difficult to value, companies in the artificial intelligence universe. Its business combines mission-critical software for governments, data platforms for enterprises, and a new layer of enterprise AI through AIP. The company is growing at exceptional rates, with accelerating revenue, expanding margins, strong cash flow generation, and a virtually debt-free balance sheet.

The most compelling aspect of this thesis is that Palantir isn’t just competing to sell AI models, but to become the operational layer that connects data, permissions, processes, and real-world decisions within complex organizations. If AIP manages to establish itself as a key infrastructure for businesses and governments, the potential addressable market could be enormous.

The problem is the valuation. Even assuming high growth, very high margins, and above-average cash conversion for traditional software, the current price seems to discount a very optimistic scenario. In my model, my base-case intrinsic value estimate of $48 per share falls well below the market in the base case scenario and only approaches the current price under assumptions closer to the best case.

My opinion is that Palantir is a very high-quality company, with a very attractive strategic position within enterprise AI, but the stock seems very expensive to me even despite the recent declines.

Introduction

Palantir Technologies is one of the most controversial software companies currently listed on the Nasdaq, and also one of the most difficult to value using traditional tools. Founded in 2003 by Peter Thiel, Alex Karp, Joe Lonsdale, Stephen Cohen, and Nathan Gettings, it was established with a very specific goal: to help the U.S. intelligence community integrate and analyze scattered data after the September 11 attacks, with initial backing from In-Q-Tel, the CIA’s venture capital arm. More than twenty years later, that same architecture of data integration, semantic modeling, and artificial intelligence has become a platform that sells solutions to the Pentagon and U.S. and allied intelligence agencies, as well as to insurers, banks, airlines, hospitals, and industrial manufacturers.

The correct way to analyze it is not as a defense company, nor as a simple analytics software provider, but as a decision infrastructure: a system that connects raw operational data (sensors, transactions, logistics records, intelligence reports) with a semantic model (the “ontology”) upon which applications, operational workflows, and, since 2023, large language models run through its Artificial Intelligence Platform (AIP). This ontology, according to the company’s own thesis, is what differentiates Palantir from a simple data repository: it transforms a row in a database into a real-world concept (a “tank” with a fuel level and location, or a “customer” with a payment history and fraud risk) upon which AI can reason and act with traceability and control.

The first quarter of 2026 confirmed that the company is experiencing its own tipping point for generative AI, with two years of cumulative adoption since the launch of AIP. Revenue reached $1.633 billion, an 85% year-over-year increase, the highest growth rate in its history as a public company. The commercial business in the United States grew 133% year-over-year, and the US government business grew 84%. The adjusted operating margin for the quarter was 60%, and the Rule of 40 (the sum of revenue growth and operating margin, a standard quality indicator for software companies) reached 145%, a combination that, according to management, is comparable only to that of other AI infrastructure companies such as Nvidia, Micron, or SK Hynix.

The stock traded above $207 at the end of 2025 and, by the end of June 2026, it was in the $106–$113 range, a decline of more than 45% from its 52-week highs, amid a widespread correction in artificial intelligence stocks, sustained selling of shares by founders and executives, and media coverage of Michael Burry’s short position.

In this report we will examine the business model and its various layers (Gotham, Foundry, Apollo and AIP), the historical and recent financial performance with its corresponding vertical and ratio analysis, the management team and corporate governance structure, the company’s specific regulatory and reputational risks, the competitive landscape under the framework of Porter’s five forces, a SWOT analysis, and finally a discounted cash flow valuation constructed with three scenarios (Best, Base and Worst Case) and two terminal value methods, along with a conclusion on what assumptions are needed to justify the current share price.

Business model

Palantir’s business model combines software subscriptions, long-term contracts, expansion within existing clients, and services necessary to implement solutions in complex environments. Unlike a traditional horizontal SaaS, Palantir doesn’t typically sell a simple tool that a customer can simply activate with a credit card. The sale usually stems from a specific operational problem: integrating data, building an ontology ( creating a “logical map” of how a company works) , connecting systems, improving a critical decision, or automating a process with AI.

This characteristic gives Palantir a unique dynamic. On the one hand, sales cycles can be longer, and implementation may require close collaboration with the client. On the other hand, once the platform is integrated into critical processes, switching costs can be very high. If Foundry, Gotham, or AIP become part of an organization’s nervous system, operational dependence can be significant.

The model typically progresses in three stages. First, Palantir enters with a limited use case, where it attempts to demonstrate rapid value. Then, if that use case is successful, it expands the platform to other areas of the client’s business. Finally, in the best-case scenarios, the platform becomes a cross-cutting layer upon which applications, decision flows, and automations are built. This is where the true economic power of the model emerges: landing and expanding with increasingly complex contracts.

With AIP, Palantir sought to accelerate this process through bootcamps. The idea is to move from a conceptual sale to an applied demonstration of real-world customer problems. Instead of selling the abstract promise of AI, Palantir shows how a model can interact with internal data, permissions, business rules, and possible actions. If the customer sees an impact within days, the sales conversation shifts.

The model has a very attractive financial structure as it scales. The gross margin is high, capex is low relative to sales, and the company already generates significant cash flow. This sets it apart from many more capital-intensive AI stories, such as data centers, semiconductors, or cloud infrastructure. Palantir is participating in the AI wave from a software layer, not from a physical layer that requires billions of dollars in assets.

Gotham

Gotham is Palantir’s original platform and represents the company’s origins. It is designed for government, defense, intelligence, security, and critical operations. Its primary function is to integrate data from multiple sources and enable teams with varying permissions to analyze information, detect patterns, and make coordinated decisions.

Gotham’s value lies not in visually displaying data, but in operating in contexts where data is sensitive, permissions are complex, and speed can be critical. In defense, for example, information can come from sensors, satellites, field reports, logistics, or intelligence. The challenge is not just storing that data, but transforming it into a coherent operational picture.

This business model has clear advantages. Government clients are typically hard to win, but also hard to lose once the software becomes an integral part of their operations. Barriers to entry aren’t limited to the product itself: they include authorizations, institutional trust, track record, security, integration, and process knowledge. That’s why Gotham remains a core component of Palantir’s strategy.

The risk is that government business also depends on public budgets, political cycles, administrative processes, and reputational sensitivity. Palantir operates in areas where controversy is inevitable. This exposure can be a strength when Western governments prioritize defense and intelligence, but also a limitation in certain markets or with certain clients.

Foundry

Foundry is Palantir’s bridge to the commercial world. Its goal is to enable large enterprises to integrate data, build an operational representation of their business, and develop internal applications on top of that. Foundry can be used in manufacturing, healthcare, energy, financial services, consumer goods, logistics, or any industry where operations are complex.

Foundry’s most important concept is ontology. Palantir uses this word to describe a digital representation of the business: products, customers, plants, suppliers, contracts, orders, routes, assets, permissions, risks, and processes. It’s not simply about cleaning databases. It’s about giving meaning to the data and connecting it to how real decisions are made.

This layer is especially relevant for AI. A language model without business context can be useful for general tasks, but it can’t make decisions about inventory, margins, logistics, or customers if it doesn’t understand the organization’s internal structure. Foundry aims to be that context layer. If the ontology becomes central, the platform’s value increases, and so do the switching costs.

The business challenge is that Foundry competes in a market saturated with alternatives. Companies can use Microsoft, Snowflake, Databricks, ServiceNow, Salesforce, Oracle, hyperscalers, consulting firms, or in-house development. Palantir has to demonstrate that its operational approach generates more value than simply combining existing tools. AIP appears to have improved its proof of value, but competition will remain fierce.

Apollo

Apollo is less visible to investors, but it’s a key component. It allows for the deployment, management, and updating of software in very different environments: public cloud, private cloud, on-premises, disconnected networks, or classified systems. For a company working with defense and mission-critical organizations, this capability is no small technical detail.

Many software companies are designed to operate almost exclusively in the public cloud. Palantir cannot assume that. Its customers may have security, data sovereignty, or connectivity constraints. Apollo helps platforms run where the customer needs them, without losing the ability to be updated and maintained.

From an economic standpoint, Apollo is important because it increases the scalability of the business model. If each deployment depended on manual work, Palantir would have less room to grow without incurring additional costs. Automating deployments and updates is essential for maintaining high margins.

AIP

Generative artificial intelligence opened up a huge demand, but it also exposed a practical problem: many companies can test models, but few can put them to work in real processes, with security, permissions, auditing and the ability to act.

AIP seeks to solve that problem. The platform allows you to connect language models with internal data, ontologies, operating systems, and business rules. It also allows you to build agents, automations, and applications, but within a governed framework. For Palantir, this point is central: enterprise AI needs control, not just creativity.

A simple example helps illustrate this. A company might ask a model which plant is most at risk of delays or which supplier is causing problems. But to provide a useful answer, the model needs to know which plants are involved, what orders are pending, what inventory is available, which contracts apply, what permissions each user has, and what actions can be taken. AIP aims to bring AI down to that level of context.

AIP’s bootcamps also changed the go-to-market approach. Palantir doesn’t expect customers to fully understand the architecture before purchasing. It aims to demonstrate value quickly with a real-world use case. This reduces the time between initial curiosity and implementation. The growth of the US commercial segment suggests this strategy is working, although it remains to be seen how it will perform with a much larger customer base.

According to the bullish view, AIP is the piece that transforms Palantir into a core enterprise AI platform. According to the bearish view, AIP could be a powerful but not unique layer, facing competition from Microsoft, hyperscalers, data platforms, and internal solutions. The difference between these two interpretations perhaps explains much of the current valuation.

Business quality

Sales evolution

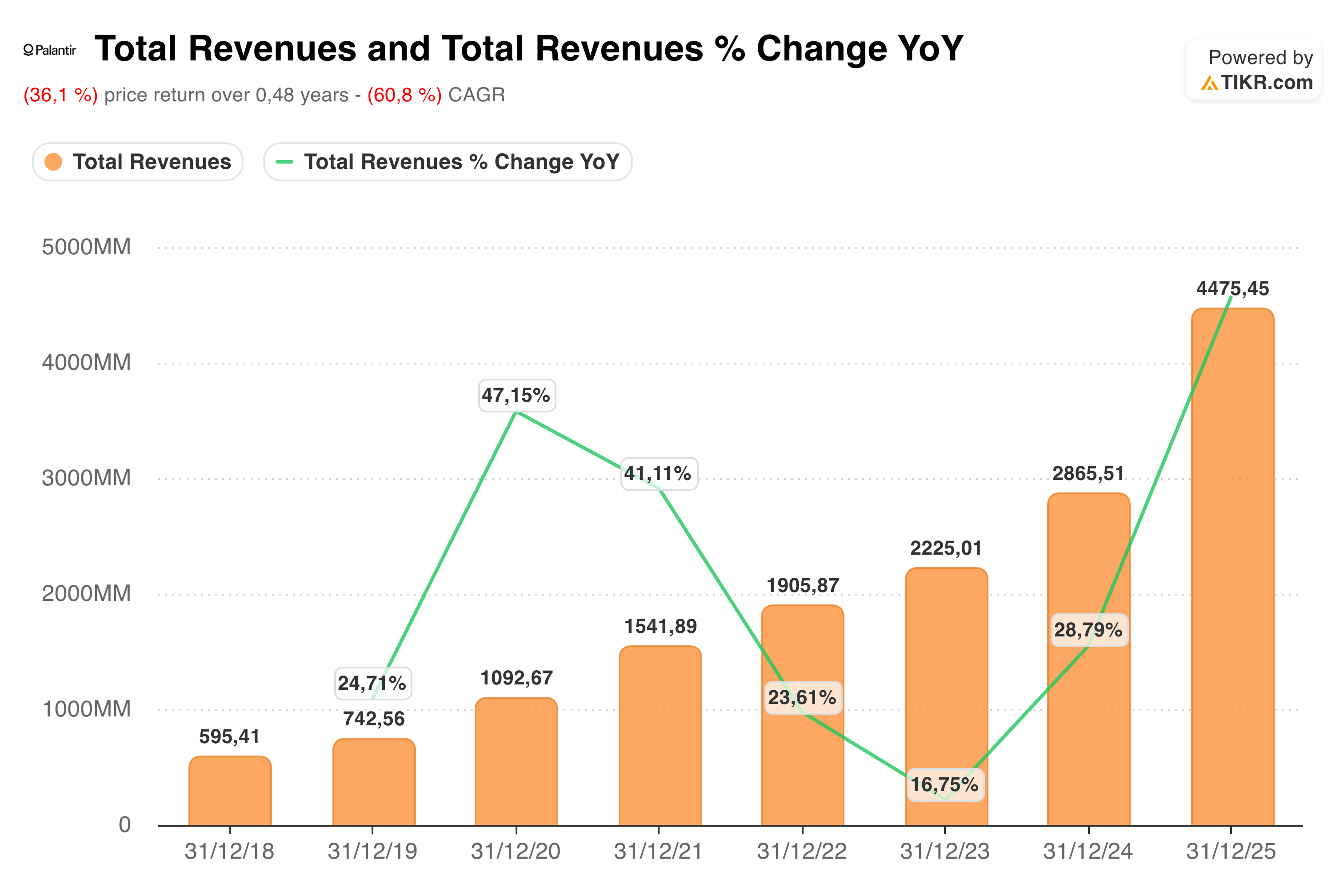

Between 2018 and 2025, Palantir’s revenue grew from approximately USD 595 million to USD 4.475 billion. This represents a more than sevenfold increase in revenue over seven years. While the growth wasn’t linear, it does demonstrate a clear trend: the company successfully transitioned from a relatively small revenue base to a significant player in the enterprise software industry.

The most striking figure is the recent acceleration. After growing 16.7% in 2023 and 28.8% in 2024, Palantir accelerated strongly again in 2025, reaching 56.2% growth. This acceleration coincides with the adoption of AIP and the explosive growth of the commercial business in the United States.

Looking ahead to 2026, both the consensus and the company’s own guidance point to another very strong acceleration. My model is based on 2026 revenues of approximately USD 7.653 billion, which implies a 71% increase compared to 2025.

Vertical analysis

Income Statement

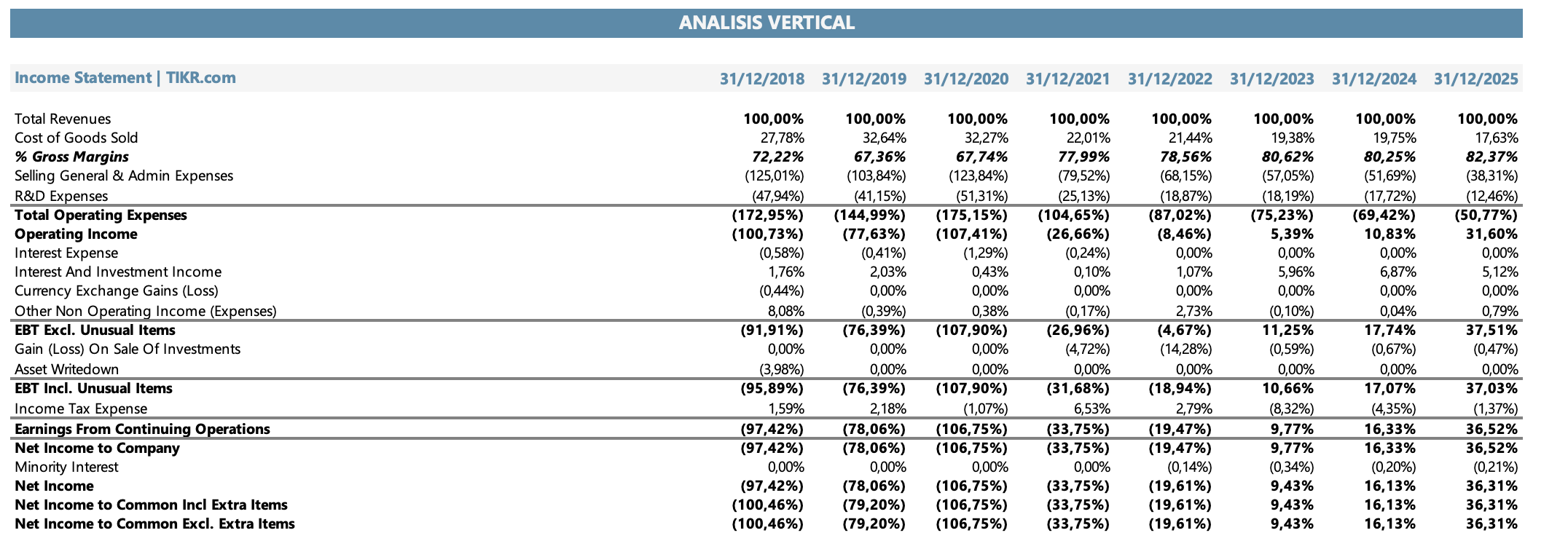

For years, Palantir had negative operating margins, partly due to commercial investment, research and development expenses, stock-based compensation, and a structure still in the process of scaling up. That stage is now increasingly behind us.

The gross margin remained high, reaching 82.4% in 2025. This is one of the most important aspects of the business. Despite the complexity of its implementations, Palantir is showing gross margins typical of a high-quality software company. This helps answer one of the long-standing questions: whether the business could scale without behaving like a consultancy. The recent answer appears to be quite positive.

The most significant change is in the operating margin. In 2021, the operating margin was negative at 26.7%. In 2022, it was still negative at 8.5%. In 2023, it turned positive at 5.4%, in 2024 it rose to 10.8%, and in 2025 it jumped to 31.6%. In Q1 2026, the GAAP operating margin reached 46%. This expansion is highly relevant because it demonstrates that the company is capturing real operating leverage.

The net margin also improved dramatically. After years of losses, Palantir achieved a net margin of 9.4% in 2023, 16.1% in 2024, and 36.3% in 2025. Part of this improvement includes financial income from the company’s large cash position and investments, but the trend in operating profitability is still difficult to ignore.

The next question is whether these margins are sustainable. In my base model, I assume that the EBIT margin reaches 38% in 2026, gradually increases to 46% in 2035, and normalizes at 45% in the final year. This is a demanding assumption, but not impossible if Palantir truly scales as a software platform with low incremental cost. The risk is that competition, the need for investment in talent, or greater implementation complexity could limit that expansion.

Balance Sheet

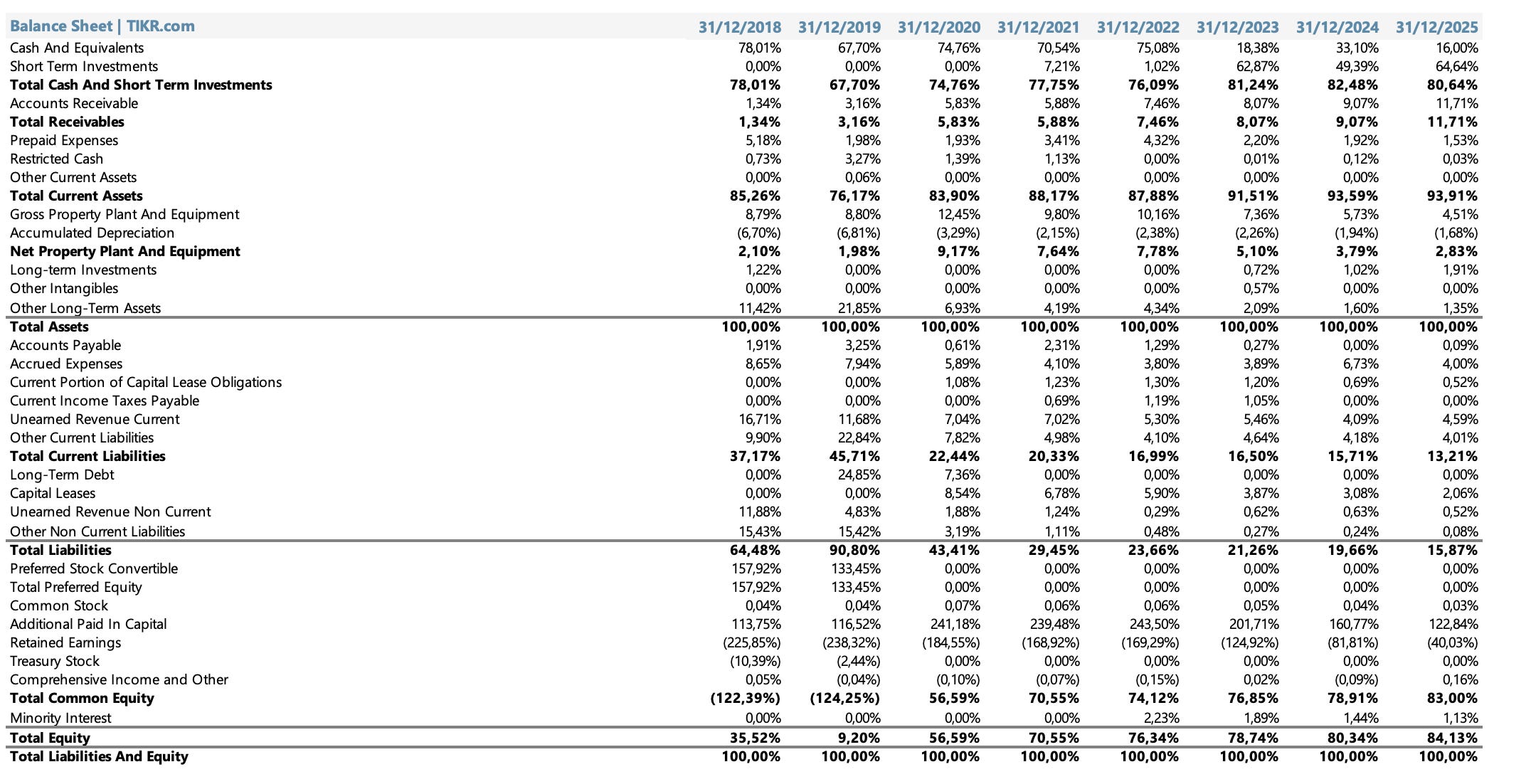

Palantir’s balance sheet is one of its strongest assets. The company ended 2025 with approximately USD 7.177 billion in cash and short-term investments, and by Q1 2026 that figure had risen to nearly USD 8 billion. Furthermore, it had no outstanding traditional financial debt. This gives it tremendous flexibility in a market where many growth companies rely on external financing.

A strong balance sheet matters for several reasons. First, it allows the company to invest aggressively in product, talent, and business expansion without relying on the capital markets. Second, it reduces financial risk in a stock that already has a long implied duration. And third, it provides the option for acquisitions, buybacks, or strategic investments should opportunities arise.

Working capital also deserves attention. In software companies with upfront contracts, deferred revenue and operating liabilities can finance part of the growth. Therefore, I included accounts receivable, accounts payable, deferred revenue/customer deposits, and accrued liabilities in the valuation.

Cash Flow Statement

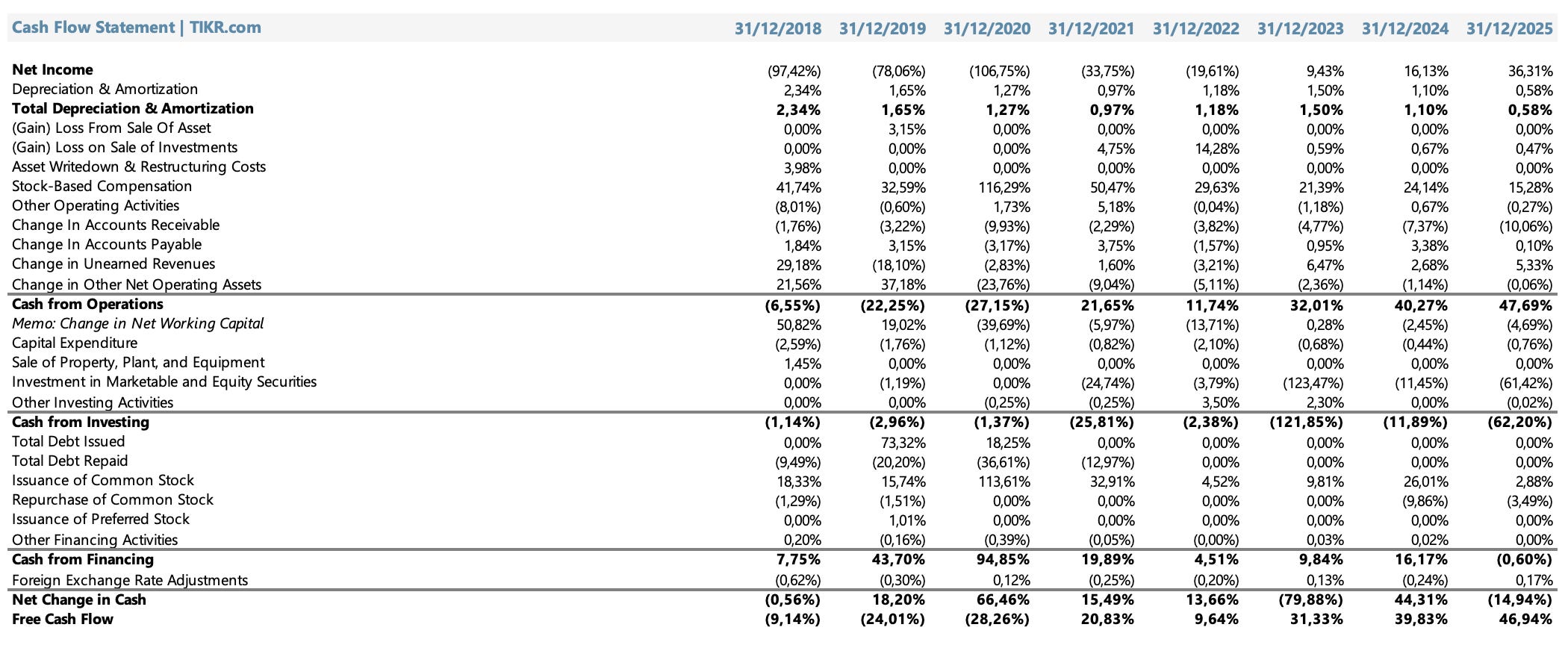

Cash generation is probably one of Palantir’s most attractive aspects. In 2025, free cash flow was USD 2.101 billion, equivalent to a margin of 46.9%. In Q1 2026, adjusted free cash flow was USD 925 million, with a margin of 57%. For a company that continues to grow at such high rates, these levels of cash conversion are exceptional.

Capital expenditures are very low compared to revenues. In 2025, capital expenditures were just USD 34 million, less than 1% of sales.

This combination of high gross margin, low capex, and favorable working capital explains why the business can generate free cash flow long before it fully matures.

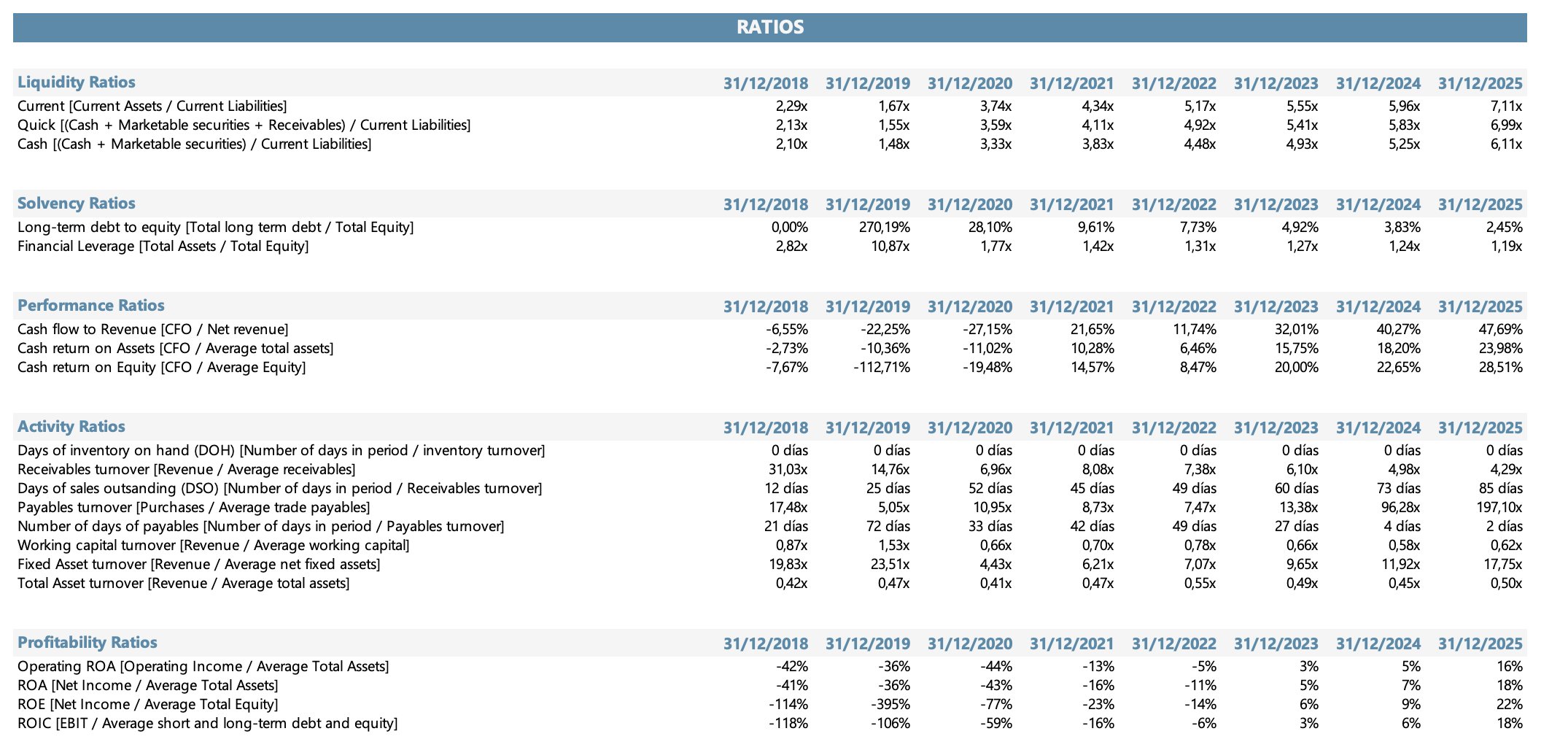

Ratios

Palantir’s ratios show a very clear improvement in the financial quality of the business. The company went from being a business with significant losses, high stock-based compensation, and negative cash flow generation, to becoming a software business with very high liquidity, almost no financial debt, and exceptional cash conversion.

In terms of liquidity , Palantir presents an extremely strong position. The current ratio increased from 2.29x in 2018 to 7.11x in 2025 , while the quick ratio and cash ratio also remain at very high levels, at 6.99x and 6.11x , respectively. This means that the company has ample capacity to cover its short-term obligations with liquid assets.

The solvency ratios reinforce this interpretation. Long-term debt to equity fell from distorted levels in 2019, when accounting equity was affected by the pre-IPO structure, to just 2.45% in 2025. Financial leverage also normalized from 10.87x in 2019 to 1.19x in 2025. This trend shows that Palantir is not growing through financial leverage. Business expansion is primarily driven by operational scale, not increased debt. For a software company with high-quality revenue, a gross margin exceeding 80%, and significant net cash, this is a very positive sign.

In performance ratios , the improvement is even more evident. Cash flow from operations as a percentage of revenue went from negative between 2018 and 2020 to reaching 47.69% in 2025. This number is very strong even by software standards. It means that almost half of every dollar of revenue is converted into operating cash before capital expenditures. The improvement is also seen in cash return on assets, which went from -10.36% in 2019 and -11.02% in 2020 to 23.98% in 2025 , and in cash return on equity, which reached 28.51% . Palantir is no longer just about growth and AI storytelling, but a company that is converting that growth into real cash.

In terms of activity ratios , the most important indicator to track is DSO, or days sales outstanding. Palantir went from collecting payments in approximately 12 days in 2018 to a range of 66-85 days in 2025. This increase warrants attention. On the one hand, it’s normal for a company scaling up with enterprise and government contracts to have longer collection periods than in its early years. On the other hand, if accounts receivable grow faster than revenue over many periods, it could signal that the company is offering more flexible commercial terms to accelerate sales. I don’t see this as an isolated red flag, but rather as one of the points that should be monitored closely. In contrast, DPO fell to just 2 days in 2025, confirming that Palantir doesn’t rely on supplier financing to generate cash.

In terms of profitability , the trend is also very positive. Operating ROA went from deeply negative levels between 2018 and 2022 to 16% in 2025. ROA reached 18% , ROE 22% , and ROIC 18% . These figures show that Palantir is already generating attractive returns on capital, which is especially important because the company maintains a huge cash position. In companies with such liquid balance sheets, ROA can be diluted by excess cash; therefore, ROIC is probably a more representative metric for evaluating the profitability of the operating business. The fact that ROIC has gone from negative to 18% confirms that the platform has gained scale and that the model has begun to show real operating leverage.

Management Team

Palantir’s founding team shows unusual continuity for a large-scale software company: Alex Karp has been CEO since 2003, Peter Thiel has been Chairman since the founding, and Stephen Cohen (original co-founder and CTO) has held the positions of President, Secretary, and board member since 2005. Joe Lonsdale and Nathan Gettings, the other two co-founders, no longer have active executive roles in the company, although Lonsdale maintains an active public profile as a venture capital investor (Eight Partners and 8VC), and Thiel, in addition to being Chairman of Palantir, heads Thiel Capital and the venture capital fund Founders Fund.

The rest of the executive team also shows unusual longevity: Shyam Sankar, Chief Technology Officer and Executive Vice President, has been with the company since 2006, holding various strategic roles over two decades; David Glazer, CFO and Treasurer, since 2013, with additional responsibility for the company’s global real estate portfolio and corporate legal matters; and Ryan Taylor, Chief Revenue Officer and Chief Legal Officer (an unusual combination of commercial and legal roles in one person), since 2010. The board of directors is composed of seven members, including the founders with Class F shares and a group of independent directors with expertise in technology, finance, and operations (among them Alexander Moore, Alexandra Wolfe Schiff, Lauren Friedman Stat, and Eric Woersching).

This continuity reduces the risk of strategic discontinuity, but it also means that the culture and execution style (strongly influenced by Karp’s public persona and the company’s origins in intelligence and defense projects) were not diluted by growth. Karp is a key figure in the company’s public narrative: a philosopher by training (with a doctorate from Goethe University Frankfurt), he often gives interviews with a provocative tone, defending Palantir’s work with Western governments as a moral stance against what he describes as the ambivalence of other Silicon Valley companies regarding national defense.

The dual-class voting structure (Class F shares held by Karp, Thiel, and Cohen) means that, in practice, no institutional investor, no matter how much capital they contribute, can alter the company’s strategic direction against the founders’ wishes.

Compensation, dilution, and insider activity

This is where special attention should be paid. Stock-based compensation (SBC) expenditure for fiscal year 2025 was approximately USD 684 million (15.3% of revenue), coming from much higher levels in previous years as a percentage of revenue. Although that proportion is declining, it still represents a source of dilution for long-term shareholders in a company that does not repurchase shares on a scale that would offset that dilution.

Even more relevant is the pattern of stock sales by top executives and founders during 2024, 2025, and 2026. According to public records (Form 4) and specialized press reports, Alex Karp sold more than $4 billion worth of stock cumulatively since 2024, including one-off sales of between $54 and $66 million in different windows in 2025 and 2026, under pre-established 10b5-to-1 plans, and also registered intentions to sell additional shares of several hundred thousand in successive quarters. Peter Thiel liquidated positions worth more than $1 billion in 2024, sold more than 2 million shares in a single day in March 2026 at prices between $140.97 and $146.80, and recorded additional sales plans for hundreds of millions of dollars during 2026. Stephen Cohen completed a $310 million sale (the largest in his history with the company), and Shyam Sankar sold approximately $420 million since 2024.

Various estimates place net insider selling (sales minus purchases) at several billion dollars accumulated since 2024, with a ratio of shares sold to bought of approximately 9 to 1 in the most recent months of the series. The company and its defenders argue that these are mostly pre-established 10b5-to-1 plans (designed precisely to avoid discretion and the “insider” signal at the time of the sale) and that it is reasonable for founders with two decades of wealth concentrated in a single stock to diversify part of their wealth, especially after such an extraordinary revaluation as that of 2023 to 2025. Critics, on the other hand, point out that the volume and persistence of sales, coupled with compensation heavily based on SBC that the company excludes from its adjusted metrics (adjusted operating income, adjusted EPS), create an asymmetric incentive: executives capture sustained cash value while the public shareholder assumes both the valuation risk and the progressive dilution.

It is not a sign that the business is deteriorating (operating results say otherwise), but it is a factor that should be monitored with the same discipline as revenue growth, particularly because insider trading volume accelerated, not slowed, as the stock approached its all-time highs.

Competitiveness

Palantir does not compete against a single rival with the same comprehensive proposition; it competes, at the same time, on at least three different fronts, each with different players and pricing dynamics.

Data platforms and enterprise AI

Databricks and Snowflake are, according to the consensus of analysts covering the sector, the competitors with the greatest financial scale and technological overlap with Foundry. Both began as data warehouse/lakehouse platforms and have been incorporating generative AI layers (Databricks AI, Snowflake Cortex) that, in certain use cases, reduce the need for a separate ontology layer like Palantir’s. Microsoft Fabric is perhaps the most underestimated commercial threat: by bundling Foundry-equivalent functionality within the Azure enterprise agreements that most large corporations already have, it competes at a much lower marginal cost to the customer. C3.ai, with its focus on pre-built vertical applications rather than a configurable horizontal platform, attracts customers looking for a faster-to-deploy, albeit less in-depth, solution. However, its recent financial trajectory (revenues of just $250 million in fiscal year 2026, with persistent operating losses and founder Thomas Siebel’s return to the CEO role in June 2026) suggests that, unlike Databricks or Snowflake, it is failing to capitalize on the same enterprise AI demand cycle.

Defense and intelligence

In the government segment, the most interesting competitor is not a traditional software provider but Anduril, the defense company founded by Palmer Luckey. Anduril combines hardware (autonomous drones, Lattice systems) with command and control software and has been winning significant contracts since 2024-2025 with its “Replicator” program. Unlike Databricks or Snowflake, Anduril competes directly for the same type of military budget as Palantir, with a hardware and software offering that some Pentagon buyers consider more comprehensive for combat scenarios, and with a private valuation estimated at around $61 billion. Traditional defense contractors (Booz Allen, Leidos, SAIC, CACI) still maintain deep institutional relationships with government agencies and compete for the same budgets, although they generally lack a proprietary software platform comparable to Gotham.

Market size

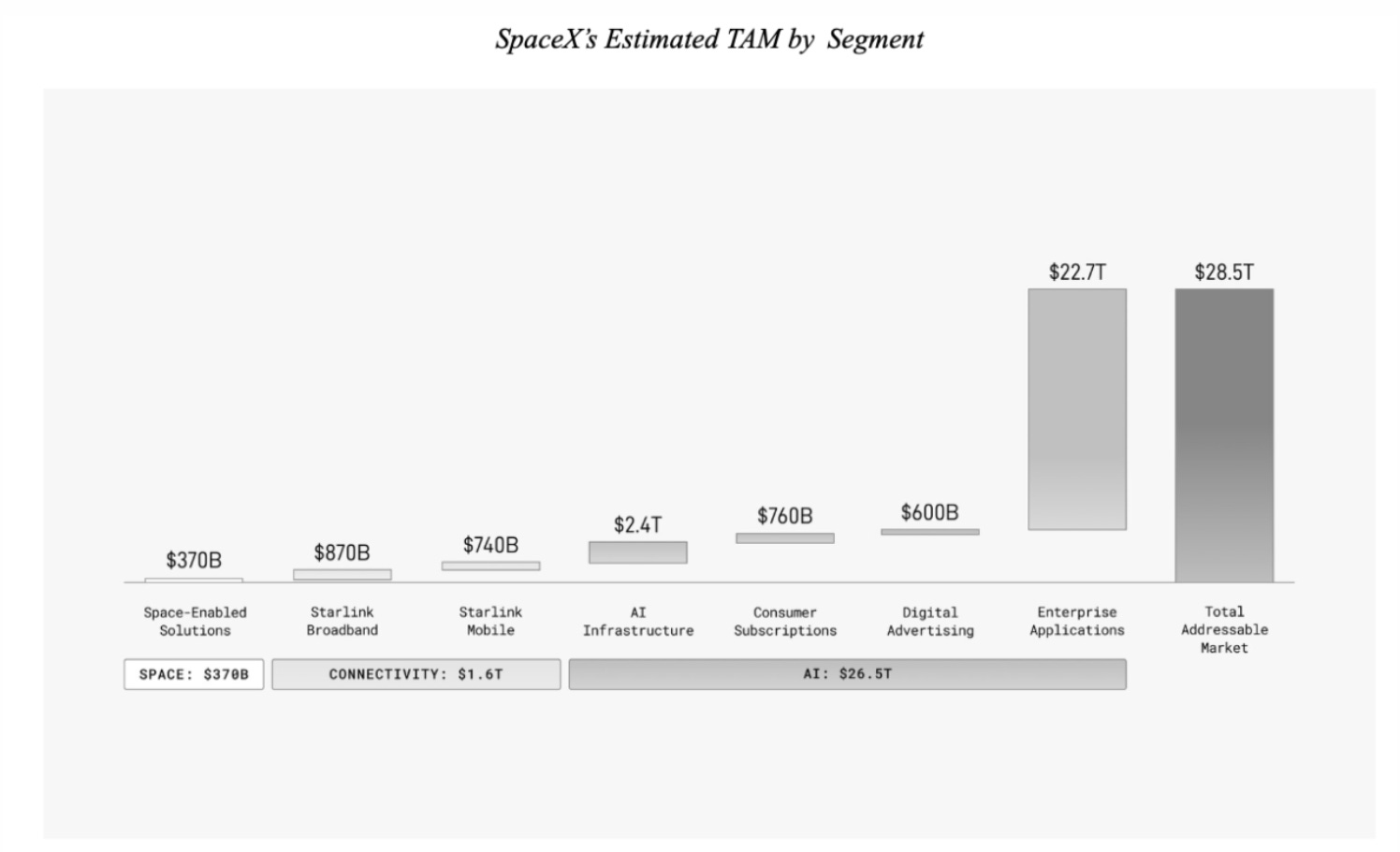

The combined Total Addressable Market (TAM) of enterprise AI and advanced data analytics has extremely disparate estimates depending on the source, so any figure should be taken with a grain of salt. PwC, for example, estimates that artificial intelligence could contribute up to USD 15.7 trillion to the global economy by 2030 , primarily through productivity improvements and effects on consumption. This TAM figure isn’t directly attributable to a company like Palantir, but it does help to put the potential size of the economic change associated with AI into perspective.

Another interesting reference appears in SpaceX’s published TAM estimates, where the company breaks down a total potential market of $28.5 trillion , of which $26.5 trillion would be linked to artificial intelligence. Within that category, SpaceX estimates $2.4 trillion for AI infrastructure, $760 billion for consumer subscriptions, $600 billion for digital advertising, and $22.7 trillion for enterprise applications. For Palantir, the relevant figure is not SpaceX’s total TAM, nor should it be interpreted as a market directly addressable by Palantir, but rather the underlying idea: a very large part of AI’s economic value could lie in enterprise applications—that is, in bringing models, data, and automation to real-world processes within organizations.

In the specific case of Palantir, I prefer to rely on a more specific definition. Morningstar estimates that Palantir’s TAM could reach approximately USD 1.4T by 2033 , within the AI ontology and orchestration platform market. This figure is much narrower than the broad estimates from PwC or SpaceX, but it is probably more useful for analyzing the market that Palantir can actually address. Even under this more specific definition, the opportunity remains enormous given the company’s current size.

If one considers the entire global AI market, the Total Addressable Market (TAM) seems virtually unlimited, but that perspective might be too broad for a serious assessment. However, if a more specific definition is used, such as ontology platforms, enterprise AI, and operational applications for large organizations, the opportunity remains substantial but allows for a more realistic analysis. In my case, I prefer to use the broader figures as context and focus primarily on a more narrowly defined target market to assess Palantir’s economic potential.

Porter’s Analysis

Competitive rivalry: high

Databricks, Snowflake, Microsoft Fabric, and C3.ai compete on the commercial front; Anduril, Booz Allen, Leidos, SAIC, and CACI compete on the government front. Palantir responds with an integrated package (ontology + AI + security accreditation) that no single rival fully replicates, but that doesn’t eliminate the pressure on price and implementation time, especially in the commercial segment, where the purchasing decision typically involves a formal competitive evaluation among several vendors.

Threat of new entrants: medium-low

Building a security-accredited ontology platform for use with intelligence agencies takes years and requires institutional relationships that are difficult to replicate; the security certifications needed to operate in classified environments represent, in themselves, a regulatory barrier to entry. The threat is greater on the commercial front, where venture-backed AI startups can offer cheaper, point-in-time solutions without needing to build a full horizontal platform, although none have yet achieved Palantir’s scale in complex operational use cases.

Supplier power: low-medium

Palantir relies on cloud infrastructure providers (AWS, Azure, Google Cloud) and, indirectly, on the availability of GPU computing capacity for its AI deployments, but as a fundamentally software company, it does not face a critical dependence on a single hardware or infrastructure provider, unlike companies that operate their own physical infrastructure on a large scale.

Customer power: medium-high

It’s high in government, where defense budgets are subject to political cycles and a client like the U.S. Army can shift entire quarters of results with a single renewal or cutback decision; it’s medium in commercial, where the cost of switching platforms increases over time as more workflows are built on the client’s ontology (known as switching cost), but the initial vendor evaluation remains competitive, and five-day bootcamps specifically aim to shorten that evaluation period before the client calmly compares alternatives.

Threat of substitutes: medium-high in generic analytics, low in more complex cases

It is medium-high in generic analytics (internal data science teams, native hyperscalers tools increasingly “good enough” for standard reporting or dashboard use cases), and low in more complex and security-sensitive use cases, where Palantir’s combination of ontology, accreditation, and operational history remains difficult to replace without a multi-year investment in equivalent capabilities.

SWOT Analysis

Strengths

Leadership in defense and intelligence software with security accreditations that are difficult to replicate; differentiated ontology platform that connects operational data with AI models in an auditable manner; AIP with explosive commercial traction and a high conversion rate from bootcamps to paid contracts; balance sheet with no significant debt and a net cash position close to USD 7.8 billion; gross and operating margins in sustained expansion since 2023; free cash flow generation well above accounting margin; stable founding team with two decades of continuity; backlog (Remaining Deal Value) growing faster than recognized revenue, suggesting visibility of future growth.

Opportunities

Continuous scaling of AI within the existing customer base, still in its early stages of penetration within each customer; a TAM of enterprise AI still in its early stages of adoption according to almost any available estimate; multi-year government contracts with greater budget predictability thanks to registration programs like Maven; expansion into NATO allies and still underdeveloped international markets within the mix; new business alliances outside of traditional verticals (Zeta Global in agentic marketing); possible flexibility in the concentration of revenue in the US as the international base matures; progressive reduction of customer acquisition cost thanks to the bootcamp model.

Weaknesses

Increasing geographic concentration in the United States (74% of revenue) and within government, around 80% in US agencies; implementation model that still relies on in-house engineers (FDEs) in the expansion phase for each client, which does not scale as elastically as pure software; steadily increasing DSO (from 12 to 66 to 85 days in seven years) with accounts receivable growing faster than revenue in most recent quarters; persistent dilution via SBC and sustained stock selling by founders and executives, accelerating rather than moderate near the stock’s all-time highs; specific reputational exposure stemming from its immigration and law enforcement contracts that does not affect most of its software peers.

Threats

Historically demanding valuations that leave very little room for error in the face of any slowdown; competition from hyperscalers (particularly Microsoft Fabric) bundling similar functionality within existing enterprise deals at a lower marginal cost; enterprise AI competitors with comparable or superior revenue growth rates (Databricks); the risk of cuts or redirections to the US and allied defense budgets; active and high-profile short positions (Michael Burry); increasing regulatory and institutional investor scrutiny (including Norway’s sovereign wealth fund) regarding the use of its tools in immigration and surveillance contexts, which could lead to future contractual restrictions or a higher reputational cost in attracting international talent and business clients; and the risk, inherent in any stock trading at extreme multiples, of an abrupt multiple compression if the market stops paying the current premium.

Valuation

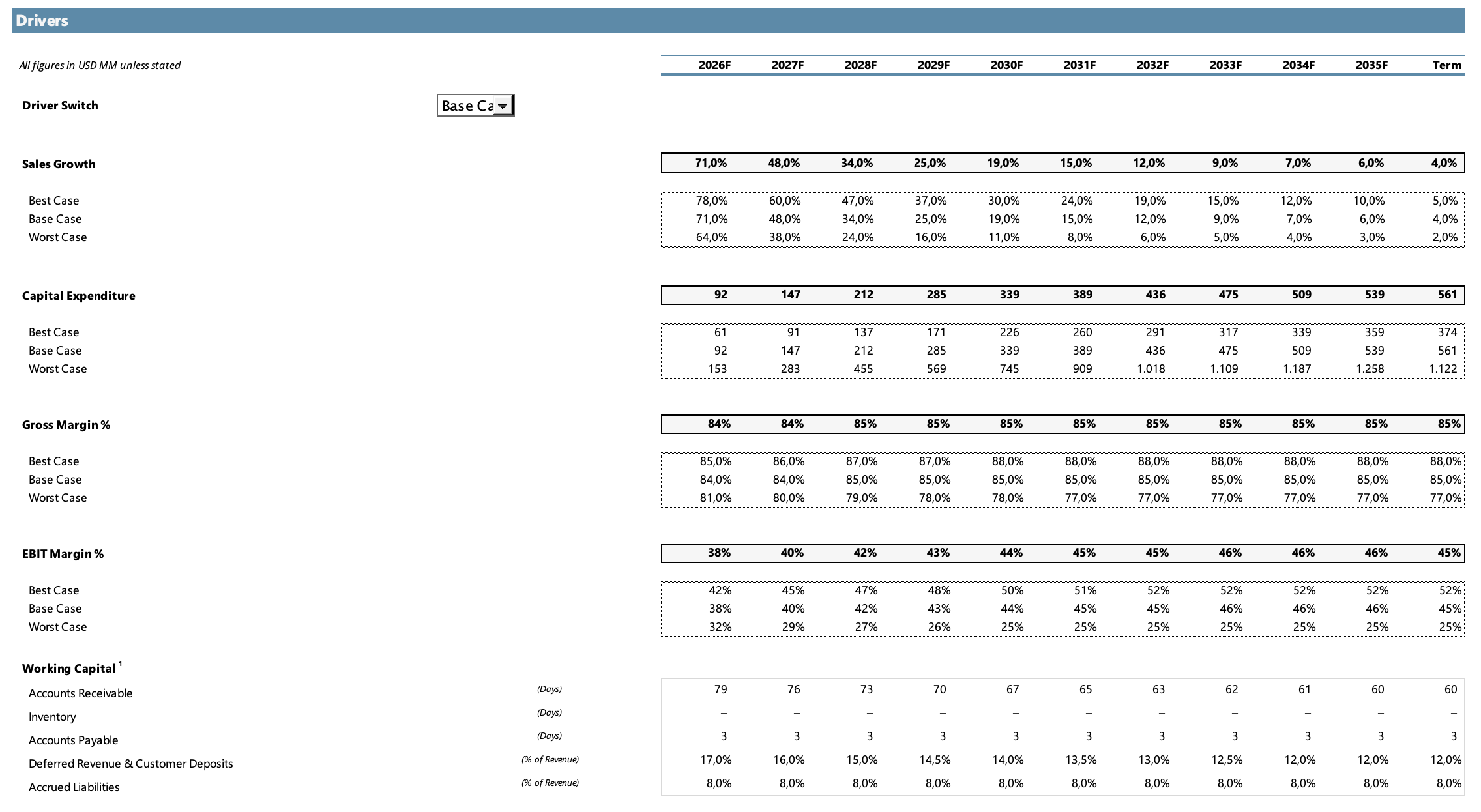

The approach used combines a perpetual growth-based DCF and an EV/EBITDA multiple-based DCF over an explicit ten-year projection period (2026 to 2035) plus a terminal year, under three scenarios (Best, Base, and Worst Case) that affect revenue growth rates, margins, and, to a lesser extent, capex. Working capital is kept consistent across scenarios, as it is not a primary driver of growth and margins for this valuation, but it was modeled with a greater level of detail, incorporating not only accounts receivable and inventory, but also deferred revenue, customer deposits, and accrued liabilities.

The two terminal value methods were weighted equally at 50%. The reason for this is that, as will be seen later, both methods yield results well below the market price in the Base scenario, and only converge close to that price in the most optimistic scenario. Inclining the weighting towards the method that yields the more generous result would not change the qualitative conclusion of the analysis, and doing so would introduce an optimistic bias that does not seem justified given how demanding the valuation starting point already is.

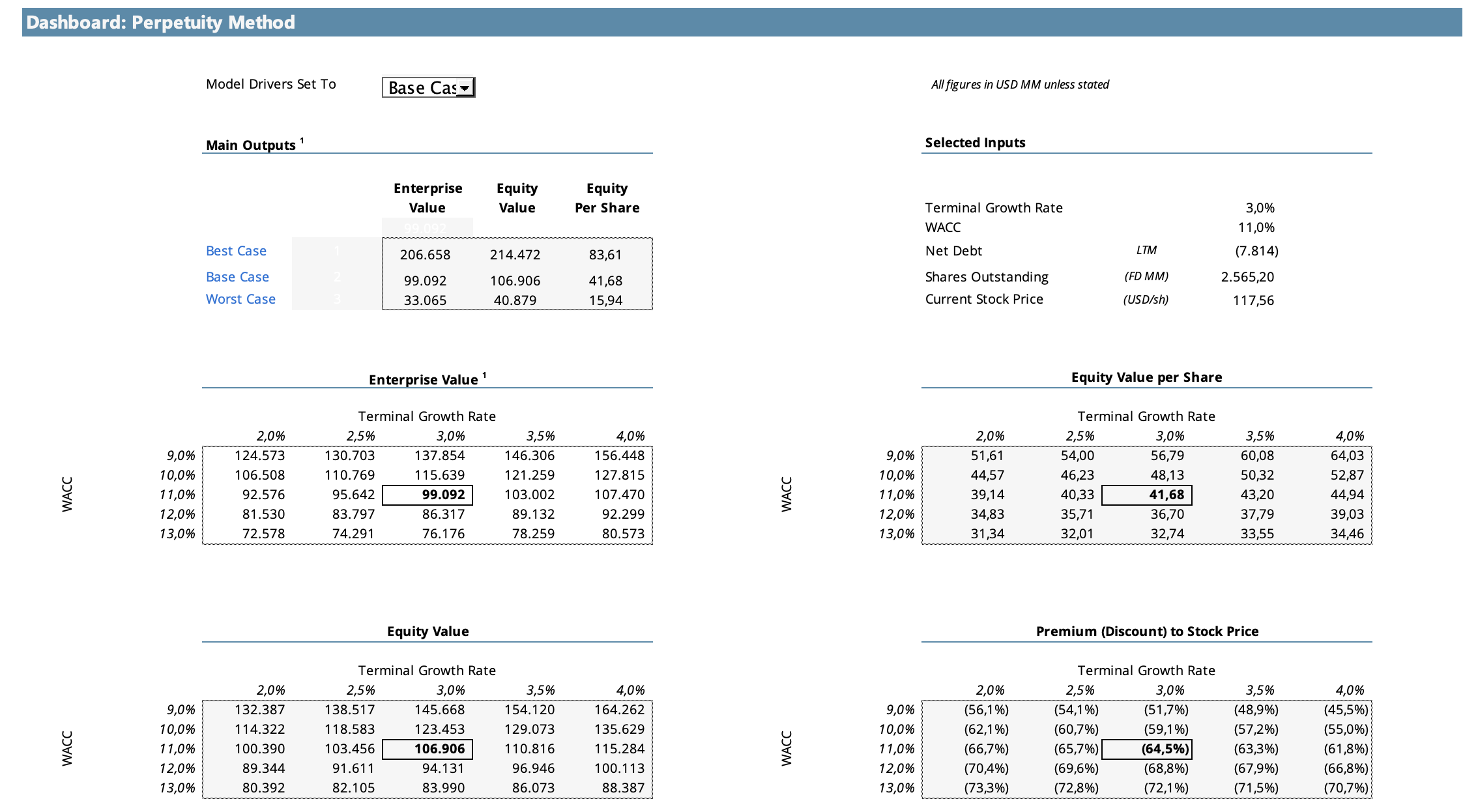

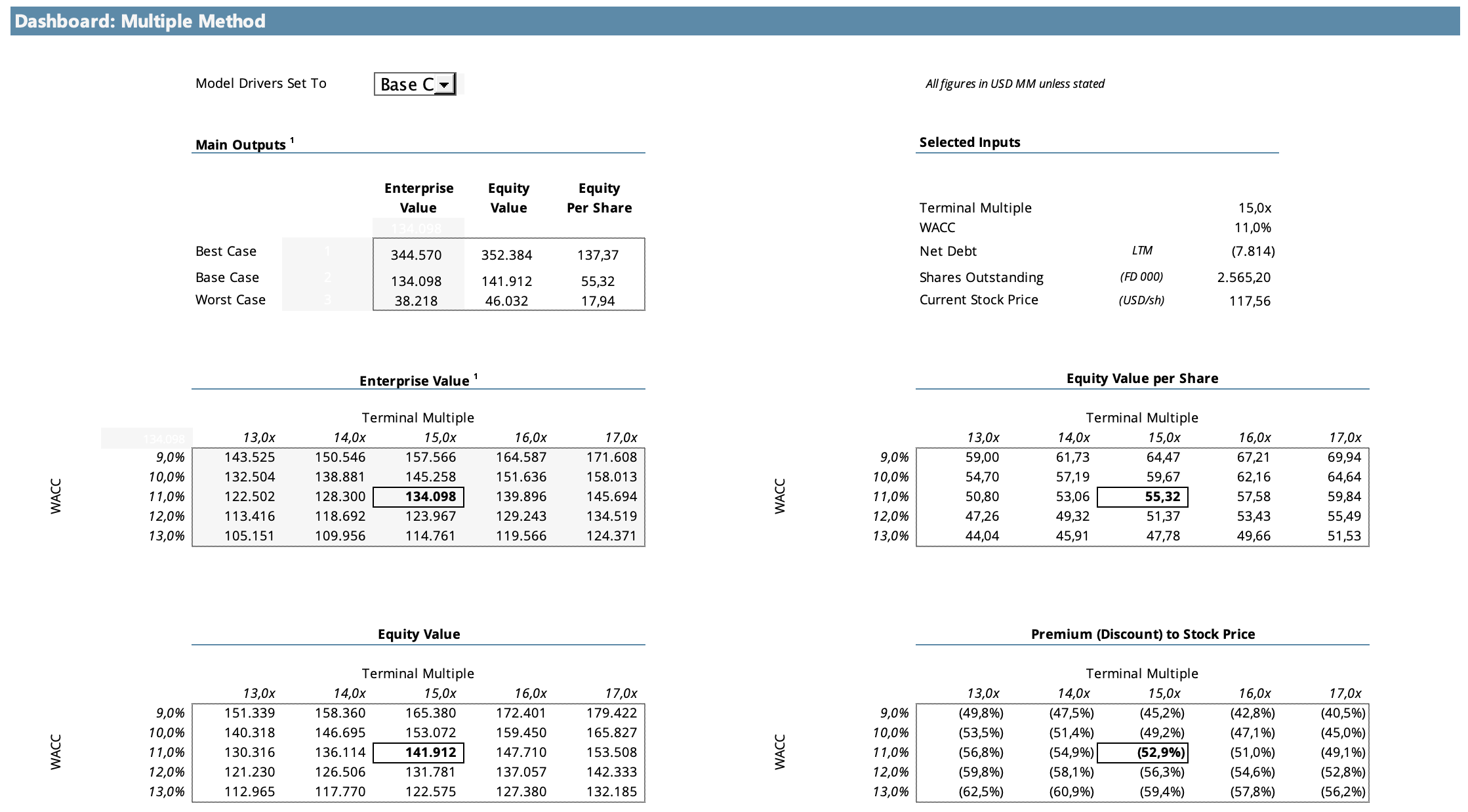

The valuation starts from a reference price of USD 112.88 per share (the stock traded in a range of USD 106 to 113 during the last week of June 2026, with a 52-week low of USD 106.37 and a high of USD 207.52), with 2,565.2 million diluted shares and a net cash position (negative net debt) of USD 7,814 million. The WACC used is 11.0% and the terminal growth rate for the perpetuity method is 3%.

Main assumptions of the model

For the valuation of Palantir, I used three scenarios: Worst Case, Base Case, and Best Case, with different assumptions regarding sales growth, gross margin, EBIT margin, and capex. The idea is not to project with pinpoint accuracy each year, something impossible in a company that is growing so rapidly and in a still-developing category, but rather to define what combination of growth, profitability, and reinvestment would be needed to justify different ranges of intrinsic value.

In Palantir’s case, the most important point is that its valuation doesn’t depend solely on the company’s growth. It also depends on that growth translating into very high margins and above-average cash conversion for traditional software. Palantir is not a capital-intensive company; it doesn’t need to build its own factories or data centers to scale, and it doesn’t have significant inventory. Therefore, the model relies primarily on revenue growth, operating margin, and free cash flow.

Sales Growth

Sales growth is the primary driver of the model. In the Base Case, I project growth of 71% in 2026 , 48% in 2027 , and 34% in 2028 , before a gradual slowdown to 6% in 2035 and 4% in the terminal period . These assumptions align with the analyst consensus for the early years, as very strong expansion is still expected during this period, driven primarily by AIP and the acceleration of the commercial segment in the United States.

The reasoning behind the Base Case is that Palantir has managed to sustain several years of high growth thanks to a combination of AI adoption, expansion into commercial clients, larger-scale government contracts, and greater penetration of its platforms in large organizations. However, I also assume that the growth rate will gradually normalize as the revenue base becomes much larger. In other words, I don’t project that the current growth will be permanent. What I do assume is that Palantir will manage to turn the current AI moment into a phase of expansion, not simply a short-term hype cycle.

In the best-case scenario, the company maintains a faster adoption rate of AIP, expands more effectively outside the United States, and establishes its platform as a critical layer for businesses and governments. In this scenario, sales continue to grow at very high rates for a longer period. In the worst-case scenario, however, the slowdown comes sooner: competition increases, customers take longer to scale implementations, and some of the current enthusiasm for AIP translates into pilot programs, but not necessarily into large, recurring contracts.

Capital Expenditure

Projected capex remains low as a percentage of sales, consistent with the nature of the business. Palantir is neither an industrial company nor a physical infrastructure company. Its model scales primarily through software, talent, third-party cloud services, and deployments on the client’s own infrastructure or external providers. Therefore, in the Base Case, capex grows in absolute dollar terms as revenue increases, but remains moderate relative to the size of the business.

In the Base Case, capex increases from approximately USD 92 million in 2026 to USD 539 million in 2035 , with a terminal value of USD 561 million . This trajectory reflects a much larger, yet still asset-light, company. In the Best Case, capex is lower as a percentage of sales because the company achieves greater operational efficiency in scaling. In the Worst Case, I assume higher capex, whether due to increased infrastructure needs, higher implementation costs, greater deployment complexity, or reduced efficiency as it attempts to expand into new customers and geographies.

The key is that Palantir doesn’t need large physical investments to grow. This is a huge advantage over other companies exposed to artificial intelligence, such as semiconductors, data centers, or energy infrastructure. The company participates in the adoption of AI, but doesn’t have to directly finance the construction of the heavy infrastructure that enables that adoption.

Gross Margin

Gross margin is one of the most important indicators for understanding business quality. In the Base Case, I assume that Palantir maintains a gross margin close to 84%-85% during the projected period, stabilizing at 85% in the long term. This level is demanding, but consistent with a high-quality software company, with low marginal delivery costs and a strong platform component.

The scenario suggests that Palantir can scale AIP, Foundry, and Gotham without direct costs growing at the same rate as revenue. The company still requires cloud infrastructure, support, implementation, and technical teams, but if the product becomes more repeatable and the bootcamps continue to reduce sales friction, the gross margin should remain at very high levels.

In the best-case scenario, I project a gross margin of 88% , which would imply an increasingly standardized platform, with a lower relative weight of services and greater delivery efficiency. In the worst-case scenario, the gross margin gradually falls to 77% , capturing the risk that Palantir will require more customized implementation, technical support, professional services, or discounts to sustain growth. For me, this risk is significant: if the company reverts to resembling a high-end technology consultancy too closely, the market should assign it a much lower margin and multiple.

EBIT Margin

EBIT margin is probably the most sensitive driver after sales growth. In the base case, I project expansion from 38% in 2026 to levels of 45%-46% in the mature stage, with a terminal margin of 45% . This is a demanding assumption, but not impossible if Palantir manages to sustain its operating leverage and if AIP becomes an increasingly scalable platform.

The logic is that sales, marketing, administration, and development expenses should grow more slowly than revenue. Palantir has already shown a very strong improvement in operating profitability, and the shift to an AIP Bootcamps business model could further improve sales productivity. If the company can convert customers faster, expand them more smoothly, and repurpose solutions across industries, the operating margin can remain at exceptional levels.

In the best-case scenario, the EBIT margin reaches up to 52% , a level reserved for exceptional software businesses with extremely high commercial efficiency and very low incremental costs. In the worst-case scenario, the margin falls to around 25% in the mature stage. This scenario reflects a world where Palantir remains a good company, but needs to invest significantly more in sales, implementation, support, and development to sustain growth. It also considers the possibility of increased competition, price pressure, or reduced real-world scalability of AIP.

Working Capital

Working capital is a particularly important factor for Palantir. For accounts receivable, I assume a gradual normalization of days sales outstanding (DSO) from 79 days in 2026 to 60 days in the long term . This reduction aims to reflect a progressive improvement in collection efficiency, although without assuming a return to the extremely low levels of the company’s early years. Palantir currently sells large enterprise and government contracts, so it makes sense that the DSO is higher than in a simple SaaS or one with small tickets.

Inventory is kept at zero because Palantir does not sell physical products. Accounts payable are kept low, around 3 days , because the company does not rely on supplier financing to operate. This is consistent with its asset-light software model.

The most relevant aspect is the inclusion of Deferred Revenue & Customer Deposits and Accrued Liabilities . In the Base Case, deferred revenue is projected to gradually decrease from 17% of revenue in 2026 to 12% in the long term . This is prudent, as it acknowledges that advance billing remains important but does not assume it will remain at excessively high levels indefinitely. As Palantir scales and changes its contract mix, some growth could come from more standardized billing arrangements.

For accrued liabilities, I maintain a stable assumption of 8% of revenue , in line with the recent business structure. This account captures accumulated operating obligations that are also part of the actual working capital dynamics. By including these two lines, the model better reflects Palantir’s cash conversion and avoids underestimating free cash flow by focusing solely on traditional accounts.

The working capital component of the model attempts to capture a simple idea: Palantir doesn’t require excessive incremental capital to grow, but it’s also unwise to assume that all future expansion will be automatically financed through deferred revenue. Therefore, I prefer a gradual normalization, especially in deferred revenue, to avoid overestimating long-term cash generation.

Perpetuity method

Under the perpetual growth method, using a WACC of 11.0% and a terminal growth rate of 3%, the estimated value per share is as follows:

The most striking result of this method is that even the Best Case (USD 80.56) doesn’t reach the reference market price (USD 112.88). Under a strict DCF reading with a conservative terminal rate, the market is demanding better performance from Palantir than my own optimistic scenario just to justify the current price, something that isn’t impossible (the company has been positively surprising quarter after quarter since 2025), but it does set a very high bar.

Even with the most favorable combination of sensitivity analysis within a reasonable range of assumptions (WACC of 9% and terminal growth of 4%), the value per share under this method does not exceed USD 64, still well below the market price. For the perpetuity method to yield a value close to the current USD 112.88, it would require combining an unusually low WACC (below 8%) with a terminal growth rate well above 4 to 5%.

EV/EBITDA multiple method

The second method uses a terminal EV/EBITDA multiple of 20x in the Best Case, 15x in the Base Case and 10x in the Worst Case, multiples anchored to high-quality mature software comparables (Microsoft, Oracle, SAP, Adobe and Salesforce are around 16x to 24x EV/EBITDA by mid-2026), not to Palantir’s current market multiple, which is around 130x EV/EBITDA and only makes sense under the assumption of sustained hypergrowth for many more years.

Here the Best Case does exceed the market price (USD 137.37 vs. USD 112.88, a 22% upside), which confirms that the current stock price is, at a minimum, discounting a combination of sustained growth and exit multiple that is located between the Base Case and the Best Case under this method, not a deterioration scenario, but a scenario that requires almost everything to go well for a full decade.

Even with a generous 20x terminal multiple (higher than virtually any mature software comparable), Base Case, with a WACC of 11%, barely reaches $66 per share, still 41% below the reference market price. Only by combining a low WACC (9%) with the most generous multiple in the range (20x) does one arrive at a value close to $77-78, which still falls short of the current price.

weighted target price

Weighting both methods at 50%, the estimated value per share is as follows:

Best Case USD 109

Base Case USD 48

Worst Case USD 17

Against the reference price of USD 112.88, the weighted Base Case target (USD 47.83) implies a downside of approximately 58%. Even the weighted Best Case target (USD 108.97) falls just short of the current price. In other words, under the assumptions of this model, the company would need to perform at the high end of the optimistic scenario for ten consecutive years just for the current price to be, at best, roughly settled, with no additional upside potential.

Conclusion

I think we all knew the conclusion of this valuation beforehand: Palantir is trading at an excessively demanding valuation. Under neither of the two methods used (neither the perpetuity method nor the multiple exit method) does the Base scenario come close to the current market price. Only in the most optimistic scenario, and only under the multiple method, does the estimated value exceed the share price, and even then, only by a moderate margin (22%). In all other possible combinations within a reasonable range of assumptions, the model suggests that the stock is trading well above what its prudently discounted future cash flows seem to justify.

The current price requires a set of very specific assumptions to be validated: that AIP growth in the commercial segment continues to sustain rates of 70 to 85% year-over-year for several more years before slowing significantly; that the operating margin continues to expand towards the 45 to 52% range without competition from Databricks, Snowflake, Microsoft Fabric, or Anduril eroding that profitability; and that, by the end of the year, the market is still willing to pay a high multiple for a company that by then would be much larger and, presumably, more mature and with a growth profile more like that of any other large-scale software company.

None of those three assumptions are unreasonable individually (in fact, the last five quarters are consistent with that trajectory, and the backlog (Remaining Deal Value) growing faster than recognized revenue suggests that the acceleration still has fuel), but the combination of the three, sustained simultaneously for ten years, is too demanding.

The risks that could disrupt this trajectory are not hypothetical either. On the financial front: the DSO has been steadily rising (from 12 to 66 to 85 days in seven years), the company acknowledges a structural shift toward revenue in arrears, and key executives and founders have been systematically selling billions of dollars’ worth of shares at a pace that has accelerated, not slowed, near the stock’s all-time highs. On the commercial front: almost 80% of the government segment relies on defense budgets from a single country, and competitors with significantly larger R&D budgets (Microsoft, the investors behind Databricks) are increasingly bundling similar functionality into products already installed in their customer base. On the regulatory and reputational front: the growing pressure from human rights organizations and institutional investors (including Norway’s sovereign wealth fund) on the company’s contracts with US immigration enforcement introduces a qualitative risk that is not common in the rest of the listed enterprise software, and whose financial materialization, if it occurs, is difficult to quantify in advance.

In support of the thesis, the balance sheet is exceptionally strong (net cash of USD 7.8 billion, virtually zero debt), the operating leverage is real and has been demonstrated quarter after quarter since 2023, and the company occupies a position that, in the most critical national security use cases, today has no obvious substitute; no competitor combines, at the same time, the security accreditation, the operational track record, and the depth of the ontology layer that Palantir built over two decades.

In short, I don’t think Palantir is a bad investment. However, the current share price already incorporates a high probability that this exceptional quality will be maintained for a full decade, leaving little room for safety if reality ends up resembling the Base Case scenario more than the Best Case scenario. Personally, I don’t own any shares in the company, and I wouldn’t feel comfortable opening a position despite the sharp drop from its highs, as the valuation remains very demanding.

Thank you so much for reading.

Alan